Finally here is an easy to follow, comprehensive, well researched, and unbiased paper from FRBNY (Tobias Adrian and Adam Ashcraft) on the so-called shadow banking (many thanks once again to Kostas Kalevras for pointing it out). A few comments:

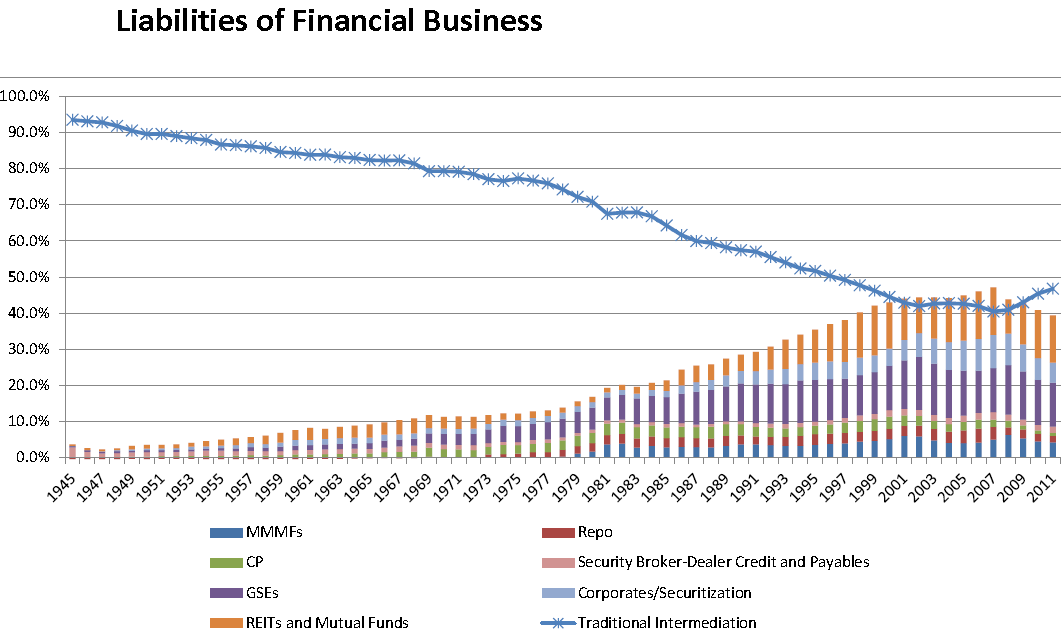

I. This chart from the paper shows the breakdown of the "traditional" vs. the "shadow" banking market sizes. It is important to point out the precise definition of traditional banking sources of funds.

Traditional Intermediation [sources of funding] refers to net interbank liabilities [banks borrowing from each other] plus checkable and savings deposits of depository institutions plus reserves of life insurance companies and pensions plus [unsecuritized] corporate debt.

|

| Source: FRBNY (click to expand) |

Note that a big chunk of shadow banking is comprised of the GSE (Fannie Mae, Freddie Mac), something the mainstream media often misses. Also this does not include government sponsored student loans, which many would classify as shadow banking (and could become a serious issue at some point).

II. The authors may have overemphasized the complexity of the securitization process with the 7 steps (chart below). Yes, in the few years leading up to the financial crisis, with CDO squared, etc., one could potentially count this many steps. But those days are over. Modern securitization usually involves only the first three steps. For example, in CLOs one has the following:

- Banks lend to corporations and syndicate those loans.

- The CLO manager uses a "warehouse line" to purchase some large portion of the loans needed for the CLO.

- A permanent entity is set up, which issues the liabilities (tranches) and buys the loans out of the warehouse. It than uses excess cash from issuing the tranches to buy more loans in the market.

ABS deals (autos, cards, etc.) also have three steps and are even simpler. The use of ABCP has declined dramatically and with it went some of the more complex securitization (see discussion).

|

| Source: FRBNY (click to expand) |

III. The authors also put too much emphasis on regulation. Investors need to do their own homework rather than relying on rating agencies as they often did prior to 2008 (rating agencies had some serious conflicts of interest - also discussed in the paper). If a sophisticated investor buys a complex bond without understanding the risks, it has to be his/her problem. The government should stay out of it because in trying to protect such investors the authorities will create moral hazards. Plus the fact that something is regulated doesn't make it a safe investment by any stretch. There are plenty of "regulated" stocks and ETFs out there that could do serious damage to one's portfolio. Regulation of shadow banking should be limited to how it impacts regulated banks (such as not allowing Citibank or Wachovia to run a massive off-balance-sheet portfolio via CP conduits with a relatively small regulatory capital allocation - regulatory capital arbitrage). Assigning appropriate levels of capitalization to liquidity backstops and credit guarantees is where the focus should be.

The other type of regulation that would be helpful is in products that are marketed and sold to retail investors/borrowers. For some reason mortgage brokers do not have to have the same level of regulatory scrutiny and licensing requirements as securities brokers. Yet for many households a mortgage is a much more risky transaction than their securities purchases (see discussion) - as we have discovered during the financial crisis.

IV. What many people (particularly the mass media) don't fully appreciate is that much of the securitization activities - which if done properly can be extremely helpful to the US consumers and to the economic growth as a whole - were started by the US government.

FRBNY: - In many ways, the modern shadow banking system originated in the government sector. Securitization was first conducted by government-sponsored enterprises (GSE), which are comprised of the FHLB system (1932), Fannie Mae (1938), and Freddie Mac (1970). The GSEs have dramatically impacted the way in which banks are funded and the way in which they conduct credit transformation: The FHLBs were the first providers of term warehousing of loans, and Fannie Mae and Freddie Mac pioneered the originate-to-distribute model of securitized credit intermediation.

Like banks, the GSEs fund their loan and securities portfolios with a maturity mismatch. Unlike banks, however, the GSEs are funded not through deposits, but through capital markets, where they issue short- and long-term agency debt securities. These agency debt securities are bought by money market investors and real money investors such as fixed-income mutual funds. The funding functions performed by the GSEs on behalf of banks and the way in which GSEs are funded are the models for wholesale funding markets. The GSEs use several securitization techniques. They use term loan warehousing services provided by the FHLBs. They also use credit risk transfer and transformation through credit insurance provided by Fannie Mae and Freddie Mac. Securitization functions are provided by Fannie Mae and Freddie Mac. Maturity transformation is conducted on the GSEs’ balance sheets through retained portfolios. These securitization techniques first used by the GSEs were adopted and imitated by banks and nonbanks to generate the nongovernmental shadow banking system. The adaptation of these techniques gave rise to the securitization-based, originate-to-distribute credit intermediation process.

Enjoy!

Shadow Banking - Dan Freed, you'll appreciate this one.

SoberLook.com